Overview of 2014 Tax Increase Prevention Act

December 18, 2014

Donating to Legitimate Charitable Organizations

August 18, 2015

RETAIL CHANGES EFFECTIVE JANUARY 1, 2015

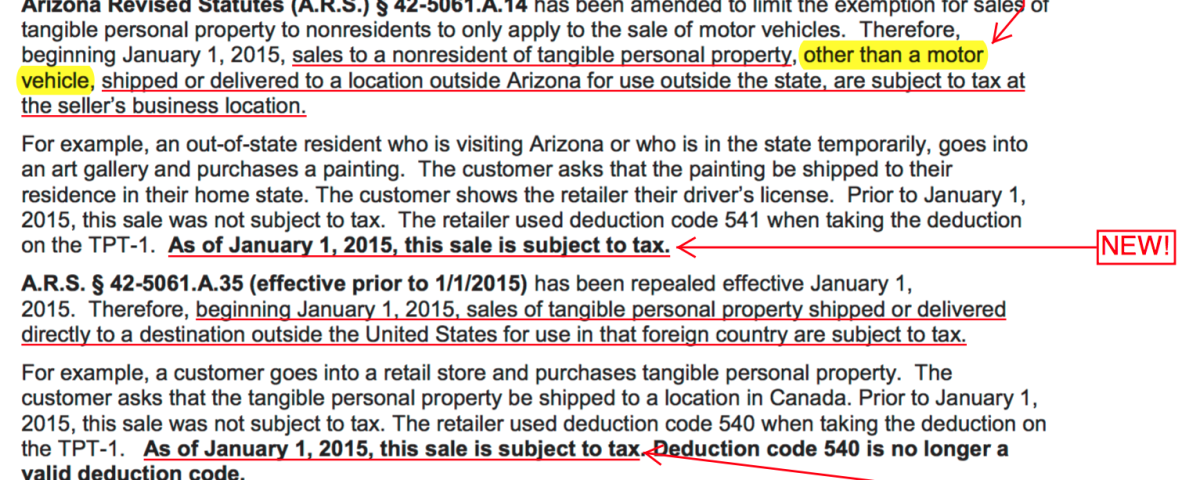

Arizona Revised Statutes (A.R.S.) § 42-5061.A.14 has been amended to limit the exemption for sales of tangible personal property to nonresidents to only apply to the sale of motor vehicles. Therefore, beginning January 1, 2015, sales to a nonresident of tangible personal property, other than a motor vehicle, shipped or delivered to a location outside Arizona for use outside the state, are subject to tax at the seller’s business location.

For example, an out-of-state resident who is visiting Arizona or who is in the state temporarily, goes into an art gallery and purchases a painting. The customer asks that the painting be shipped to their residence in their home state. The customer shows the retailer their driver’s license. Prior to January 1, 2015, this sale was not subject to tax. The retailer used deduction code 541 when taking the deduction on the TPT-1. As of January 1, 2015, this sale is subject to tax.

A.R.S. § 42-5061.A.35 (effective prior to 1/1/2015) has been repealed effective January 1,

2015. Therefore, beginning January 1, 2015, sales of tangible personal property shipped or delivered directly to a destination outside the United States for use in that foreign country are subject to tax.

For example, a customer goes into a retail store and purchases tangible personal property. The customer asks that the tangible personal property be shipped to a location in Canada. Prior to January 1, 2015, this sale was not subject to tax. The retailer used deduction code 540 when taking the deduction on the TPT-1. As of January 1, 2015, this sale is subject to tax. Deduction code 540 is no longer a valid deduction code.

However, the above amendments do not affect sales made in interstate or foreign commerce that are deductible under A.R.S. § 42-5061.A.24. If the order for the tangible personal property is received from a location outside the state and the tangible personal property is shipped or delivered by the seller to a location outside the state, the sale is not subject tax.

For example, a retailer receives a call from a customer in Ohio. The customer orders/purchases tangible personal property to be delivered to the customer in Ohio. The gross receipts from this sale are deductible under A.R.S. § 42-5061.A.24. The deduction would also apply if this order had been placed on the retailer’s website.

Arizona Administrative Code rule R15-5-170 addresses the application of this deduction.

R15-5-170. Interstate and Foreign Transactions

A. Gross receipts from sales of tangible personal property made in interstate or foreign commerce are deductible from the tax base if all of the following apply:

1. The order is received from a location outside of Arizona; and

2. The retailer ships or delivers the tangible personal property to a location outside of Arizona for use outside of Arizona.

B. In meeting the above requirements, if delivery is made by the retailer to a common carrier for transportation to a location outside Arizona, the common carrier is deemed to be the agent of the retailer for purposes of this rule regardless of who is responsible for payment of the freight charges.

C. Suitable records shall be kept to substantiate the deduction for a sale made in interstate commerce. As such, records shall identify the tangible personal property sold and the delivery destination. The following records may be sufficient to substantiate the exemption:

1. Suitable records for substantiating the receipt of an order from out-of-state may include purchase orders, letters, or written memoranda on the receipt of orders placed by telephone.

2. Suitable records for substantiating out-of-state shipments include:

a. Internal delivery orders supported by receipts of expenses incurred in delivering the property and signed on the delivery date by the person who delivers the property;

b. Common carrier’s receipt or bill of lading;

c. Parcel post receipt;

d. Export declaration;

e. Receipt from a licensed broker; or

f. Proof of export or import signed by a customs officer.

{kind=link}